Online grocery delivery in Thailand has moved from a pandemic-era convenience to a mainstream daily habit, particularly across Bangkok and the major urban provinces. The country’s quick-commerce market has evolved from a niche, urban-centric segment into a mainstream channel integrated with food delivery and modern retail, and the numbers reflect that shift — the grocery delivery segment was projected to grow nearly 19% in 2025 alone, with average revenue per user already approaching USD 190. What’s interesting about the Thai market is its structure: rather than being dominated by Western-style dark-store operators like Gorillas or Getir, growth here is anchored in super-apps and hybrid retail models that turn existing store networks into micro-fulfilment nodes. After Foodpanda’s exit in May 2025, the competitive field consolidated around LINE MAN Wongnai, GrabMart, and Robinhood Mart on the platform side, with 7-Eleven, Lotus’s, Big C, and Tops dominating the retailer-led channel. Heading into 2026, this is no longer a question of whether Thai consumers will order groceries online — it’s a question of which app they’ll open first. And for most urban Thais, that decision now comes down to two names: LINE MAN Mart and GrabMart.

How Thailand Stacks Up Against Its ASEAN Neighbours

Zoom out across Southeast Asia and Thailand looks unusual rather than typical. Indonesia remains the region’s largest food and grocery delivery market by GMV at roughly USD 6.4 billion in 2025, ahead of both Thailand and Singapore — but on growth, the story flips: Thailand emerged as the fastest-growing market in the region at 22%, partly fuelled by the government’s “half-half” co-payment scheme. The competitive shape is also strikingly different. In Malaysia, the Philippines, and Singapore, Grab commands roughly two-thirds of the market on its own, leaving challengers to fight for scraps. Indonesia is a three-way contest between Grab, GoFood, and ShopeeFood, while Vietnam has settled into a tight Grab vs ShopeeFood duel. Thailand is the outlier — the only ASEAN market where a homegrown super-app has not just survived against Grab but matched it. Following Foodpanda’s exit in May 2025, Grab and LINE MAN now control nearly 90% of the Thai market between them, splitting it close to evenly rather than ceding it to the regional giant. That’s why a Thailand-specific comparison matters: in most of ASEAN, “which grocery app should I use” is a rhetorical question.

The Market Share Picture in Thailand

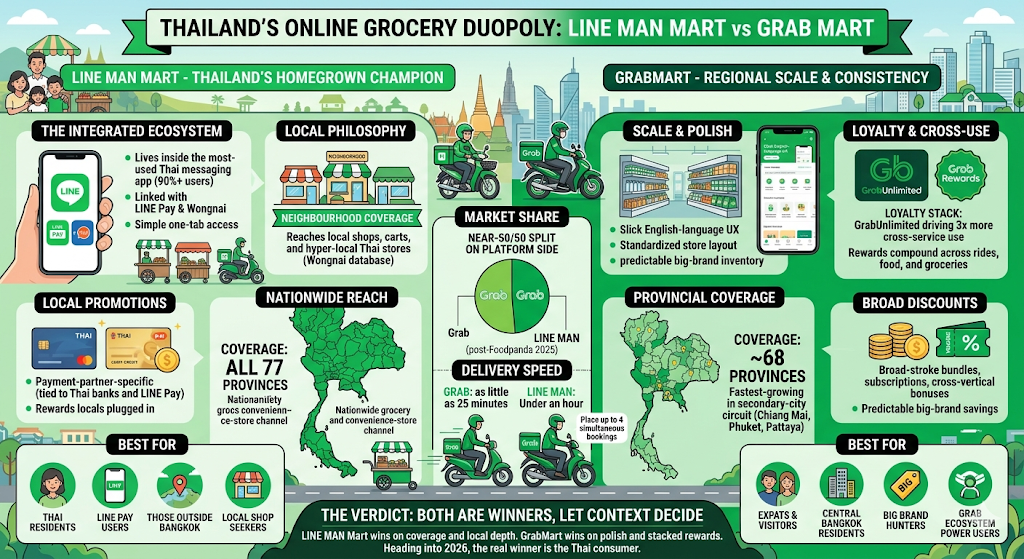

Thailand’s online grocery delivery market splits into two camps that don’t always show up on the same chart: super-app platforms and retailer-owned apps. On the platform side, the post-Foodpanda landscape is essentially a duopoly. Following Foodpanda’s exit in May 2025 — which closed after THB 13.8 billion in cumulative losses — Grab and LINE MAN Wongnai swiftly absorbed the residual demand, each retaining close to 40% of delivery transactions. Robinhood Mart sits a distant third on the platform side, and its THB 2 billion sale to Yip In Tsoi Group signalled how thin the margins have become outside the top two. The retailer-owned apps tell a different story. 7-Eleven’s “7-Delivery” service, accessible through the 7App and offering more than 15,000 items, already accounts for roughly 11% of 7-Eleven’s total Thai sales, with Lotus’s Go Fresh, Big C Online, and Tops Online filling out the supermarket-led tier. The total prize is meaningful and growing — Thailand’s quick commerce market stood at USD 0.59 billion in 2025 and is forecast to reach USD 1.01 billion by 2030 at an 11.27% CAGR — but the headline takeaway for any Thai consumer choosing an app today is simpler: if you’re not opening 7-Eleven’s own app for a top-up basket, the realistic choice is between LINE MAN Mart and GrabMart, and the two are running neck and neck.

Meet LINE MAN Mart: Thailand’s Homegrown Grocery Champion

LINE MAN Mart is the grocery arm of LINE MAN, the Thai super-app that grew out of the country’s most-used messaging platform. The strategic context matters: LINE itself is used by more than 90% of Thais and counts over 50 million users in the country, which gave LINE MAN something most regional competitors had to spend years buying — a captive, pre-installed national audience. Today, LINE MAN sits inside LINE MAN Wongnai, one of Thailand’s largest tech startups, which operates three core business groups: on-demand services under the LINE MAN brand (food delivery, mart delivery, messenger, transportation), Merchant Digital Solutions under Wongnai, and Pay & Financial Services under LINE Pay.

The Mart service itself launched in 2020 as the sixth service inside the LINE MAN app, originally powered by HappyFresh’s network of supermarkets and personal-shopper operations, and has since matured into a fully integrated grocery channel. LINE MAN MART now covers all 77 provinces, positioning it as a nationwide grocery and convenience-store delivery channel rather than a Bangkok-centric service, partnering with mini-marts, full supermarkets, fresh markets, and specialty stores. The pitch to Thai consumers is simple — you already use LINE every day, your payment is already linked through Rabbit LINE Pay, and your groceries are one tab away inside the same app.

How LINE MAN Mart Differentiates Against GrabMart

If you stand the two apps next to each other, the surface offering looks almost identical — same supermarkets, same convenience stores, same fleet of motorbike riders weaving through Bangkok traffic — but the underlying philosophies actually pull in different directions. LINE MAN Mart’s structural advantage is identity and integration: it’s an extension of the LINE ecosystem, you log in with your LINE ID, your payment auto-routes through Rabbit LINE Pay, and the same Wongnai database that powers its restaurant arm gives it deeper hooks into hyper-local Thai stores — including small carts and neighbourhood shops that aren’t formally onboarded as platform partners but get reached through its “GP Partner” commission system. That makes it feel like the Thai app — built by Thais, for Thai habits, sitting one tap away from the messaging app you already use. GrabMart’s positioning is the mirror image: scale, polish, and consistency. It’s the regional super-app, with a slicker English-language UX, a more standardised store layout, and a loyalty stack (GrabUnlimited, GrabRewards, GrabPay) that drives roughly three times more cross-service usage from members than non-members. GrabMart leans into modern-trade partnerships (big supermarkets, branded retailers), while LINE MAN Mart leans into long-tail local coverage. The pricing pitch differs too — LINE MAN’s promotions are often payment-partner-specific, tied to particular Thai credit cards or LINE Pay, which can feel less straightforward but rewards locals plugged into the right ecosystem; GrabMart’s discounts skew toward broad-stroke bundles, subscription savings, and cross-vertical bonuses (order a ride, get a Mart voucher). Practically: if you’re a Thai resident with LINE Pay set up and want neighbourhood-level coverage with the occasional under-the-radar shop, LINE MAN Mart wins. If you want a clean English interface, predictable big-brand inventory, and rewards that compound across rides and food orders, GrabMart pulls ahead.

In short, the two apps stock similar shelves, but they’re built for different shoppers. LINE MAN Mart is the local pick — it lives inside the LINE ecosystem, pays through Rabbit LINE Pay, and uses Wongnai’s database to reach small neighbourhood shops and carts that don’t show up on bigger platforms. Promotions tend to favour locals already plugged into Thai credit cards and LINE Pay. GrabMart is the regional polish play — slicker English UX, predictable big-brand inventory, and a loyalty stack (GrabUnlimited, GrabRewards, GrabPay) that rewards you across rides, food, and groceries in one go. Rough rule of thumb: if you live like a Thai, LINE MAN Mart usually wins on coverage and price; if you want consistency and stacked rewards across a super-app, GrabMart pulls ahead.

Delivery Speed and Provincial Coverage

On the surface both apps promise the same thing — your groceries at your door in under an hour — but the geography of who can actually use that promise differs sharply. GrabMart advertises delivery in as little as 25 minutes for nearby orders, with options to schedule ahead, and lets users place up to four simultaneous bookings across different stores, which is genuinely useful for a household top-up that spans a supermarket, a pharmacy, and a bakery in one go. Coverage-wise, Grab’s delivery footprint in Thailand spans roughly 68 provinces as of its last reported expansion, with the fastest-growing provincial markets being Chiang Mai, Phuket, Pattaya, Khon Kaen, and Nakhon Ratchasima — the secondary-city circuit where new middle-class demand is concentrated.

LINE MAN Mart plays a different geography game: it has expanded to cover all 77 provinces, positioning itself as a nationwide grocery and convenience-store delivery channel rather than a Bangkok-centric service. That distinction matters more than it sounds. In a tier-one area like Sukhumvit or central Chiang Mai, both apps will get a basket to you in 30–45 minutes and the difference is negligible. But in a smaller provincial town — somewhere like Nakhon Sawan, Trang, or Surin — LINE MAN Mart is more likely to actually have a partnered store within range, while GrabMart may simply not service the address. Speed in dense Bangkok corridors slightly favours Grab, since Bangkok packs more than 15,000 residents per square kilometre, creating dense delivery corridors that sustain 10-minute drop-offs and Grab’s rider density in those zones is a known strength. Outside the capital, LINE MAN Mart’s broader provincial reach is the more practical advantage. Rule of thumb: in central Bangkok, pick on price and store availability; outside Bangkok, check LINE MAN Mart first (because most likely that’s your only online grocery delivery option).

The Verdict: Which Should You Use?

Honestly, the smartest answer for most people in Thailand isn’t “pick one” — it’s install both and let context decide. The two apps are close enough on core delivery that there’s no single winner, but each has clear situations where it’s the better tool.

Use LINE MAN Mart when you’re a Thai resident with LINE Pay set up, you live outside central Bangkok, you want neighbourhood-level coverage including small local shops, or you’re hunting for promotions tied to Thai bank cards. Its 77-province footprint, Wongnai-powered local depth, and tight integration with the messaging app you’re already using make it the default everyday choice for most Thais.

Use GrabMart when you’re an expat or visitor who wants a clean English UX, you live in central Bangkok or a major tourist city where rider density is highest, you value predictable big-brand inventory, or you’re already deep in the Grab ecosystem (rides, GrabFood, GrabUnlimited) and want your rewards to compound across services. Its sub-30-minute speed in dense urban corridors and stacked loyalty programme are real advantages if you’re using Grab daily anyway. The honest summary: LINE MAN Mart wins on coverage, local depth, and Thai-resident value; GrabMart wins on polish, speed in central zones, and cross-vertical rewards. Heading into 2026, with Foodpanda gone and the market consolidated into a near-50/50 split between these two, the real winner is the Thai consumer — who finally has two genuinely competitive options and can afford to be picky about which one they open.