If you start paying attention to grocery prices in your 20s and invest the savings into a basic index fund, you retire with an extra six figures by 65. We did the math on 108 million Malaysian price records to prove it.

The two neighbours

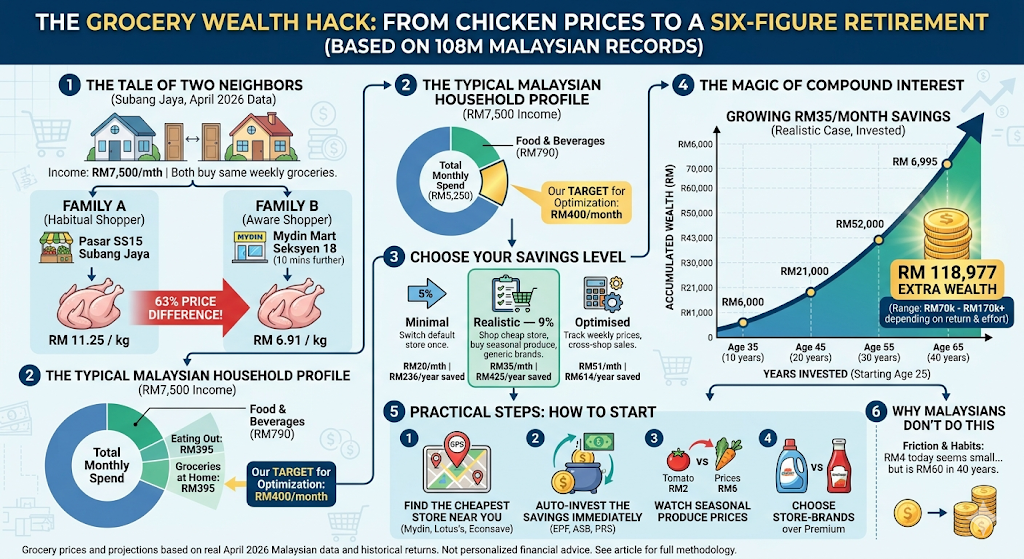

Two families live three doors apart on the same street in Subang Jaya. Both households earn around RM7,500 a month combined — both spouses working, kids in school, the typical upper-middle-class Malaysian setup. Both buy roughly the same groceries every week.

Family A drives to Pasar SS15 Subang Jaya every Saturday because they like the wet-market atmosphere. They pay RM11.25 per kilo for a whole chicken.

Family B drives ten minutes further to Mydin Mart Seksyen 18 because they noticed it’s cheaper. They pay RM6.91 per kilo for the same whole chicken.

Same chicken. Same Saturday. Same district. A 63% price difference.

Same chicken, same district, same day

Whole chicken (1kg) prices across Petaling district shops, April 2026

Both prices are real. We pulled them from the federal price-tracking system’s April 2026 data. Multiply that pattern across an entire grocery basket — eggs, vegetables, rice, sauces, household goods — across an entire month, across an entire year, across an entire working life, and the difference between Family A and Family B becomes the most consequential financial decision either of them ever makes.

Most Malaysians don’t think of grocery shopping as a wealth-building activity. They think of it as a chore. This article is about why that framing is costing you somewhere between RM70,000 and RM170,000 over your working life — purely from being a little more deliberate about where you push your trolley.

The math is genuinely shocking when you see it laid out. Let me walk you through it.

Part 1: How much your household actually spends on groceries

Before we can calculate savings, we have to be honest about the baseline. And here’s where most readers will find their first surprise: a Malaysian household earning RM7,500 a month probably spends less on groceries than they think.

Government statistics tell us this clearly. The Department of Statistics’ 2022 Household Expenditure Survey (the most authoritative source on actual Malaysian spending behaviour) found that the average Malaysian household — across all income levels — spends about 16.3% of their monthly income on food and beverages combined. But “food” includes both groceries you cook at home and the kopitiam tapao, the GrabFood, the office lunches, the weekend mamak runs.

The breakdown matters. Below is a realistic spending profile for a working couple earning RM7,500/month:

Where your RM 7,500 actually goes each month

A typical Malaysian dual-income household at this income level

If your gut reaction is “there’s no way I only spend RM400 a month on groceries” — pull your bank statements for two months and add up your supermarket receipts. Most middle-class urban Malaysian households are genuinely surprised at how much of their food budget is actually spent eating out, not buying ingredients.

For our analysis, we’ll use RM400/month as the typical groceries-at-home spend for a RM7,500-income household. That’s RM4,800 per year. It’s the number we’re going to optimise.

Part 2: The savings opportunity, item by item

Now the interesting part. We analysed every single April 2026 grocery price across more than 2,700 stores nationally — and the variance between cheapest and most-expensive shops within the same district is much wider than most people realise.

Here are some real findings from Petaling district (PJ, Subang, Shah Alam, Sunway, USJ areas) in April 2026:

- Whole chicken (1 kg): Cheapest at Mydin Mart Seksyen 18 — RM 6.91. Most expensive at Pasar SS15 Subang Jaya — RM 11.25. Spread: 63%.

- Eggs Grade A (tray of 30): Cheapest supermarket RM 9.99, most expensive RM 14.10. Spread: 41%.

- Tomato (1 kg): Cheapest hypermarket RM 0.49 (yes, really — we double-checked). Most expensive pasar mini RM 10.00. Spread: more than 20-fold.

This is the core insight: the same product, on the same day, in the same district, can cost wildly different amounts depending on where you buy it. The average household — shopping by habit, going to “their” usual store — is leaving real money on the table without realising it.

How much grocery prices vary between shops

Median spread between cheapest and most expensive shop within the same district, April 2026

When we systematically computed the gap between the cheapest store and the typical store across all 40 items in our sample basket, the median item showed a 10.1% saving if you simply default to shopping at the consistently-cheapest store in your area. The mean (which is pulled up by very-volatile items like tomato) was 14.5%. But for a fair, conservative number, let’s use the median.

Part 3: Three savings scenarios

Not everyone has the same appetite for shopping research. Some people will read this article, identify a cheaper store once, and shift their default. Others will turn grocery optimisation into a hobby. Different effort levels yield different savings.

Three savings scenarios. Pick yours.

How much you save depends on how much effort you invest. All amounts assume invested at 8% nominal returns.

Identify the cheapest hypermarket near you once. Default to it. Don’t track prices, don’t time anything.

Cheapest store + buy fresh produce when seasonally low + skip premium brands where the difference doesn’t matter to you.

Track prices weekly. Cross-shop between stores. Watch seasonal patterns. This is grocery shopping as a hobby.

For most readers, the realistic scenario is the right target. It requires no extreme behaviour change — just being slightly more deliberate about a thing you already do every week. Spend ten minutes a month thinking about it, not your weekend.

Part 4: Compound it. Now stop and look at what happens.

Here is where most articles about saving money end. The author tells you “you can save RM35 a month” and you think “ok, RM35 a month is fine but it won’t change my life.” And you stop reading.

But that framing is wrong, and it’s why most Malaysians never bother. Let me show you what RM35 a month actually becomes when you stop spending it and start investing it.

Long-term equity returns historically run around 6-8% per year depending on asset mix. Conservative for a Malaysian-only equity portfolio, possibly higher for a globally diversified one. Let’s run the numbers across multiple scenarios so you can see how sensitive the outcome is to your assumptions.

RM 35 saved monthly. Invested for 40 years.

What happens if you skip the expensive shop and invest the difference

A 25-year-old who reads this article today, makes a one-time decision to default-shop at the cheapest grocery store in their area, invests the savings into a basic index fund, and then never thinks about it again — retires at 65 with somewhere between RM70,000 and RM119,000 of additional wealth. From groceries alone. No promotion, no side hustle, no sacrifice in lifestyle. From not overpaying at the supermarket.

If they’re a more aggressive optimiser (13% savings rate), the 40-year compound figure becomes RM172,000 at 8% returns.

RM172,000 is enough to fund a house deposit, send a child through university, top up retirement, or buy a paid-off Toyota Vios in cash. And it came from no extra income — only from refusing to overpay for chicken every Saturday.

This is what compound returns do, and this is why “grocery savings” stops being an auntie budget tip and starts being a serious wealth-building tool the moment you commit to investing the difference rather than spending it.

Part 5: But it gets better — savings grow with inflation

The numbers above use a simplifying assumption: that you save RM 425 every year, exactly the same amount, for 40 years. In reality, your grocery bill grows with inflation, and so does your savings opportunity.

If you assume Malaysian grocery prices grow at roughly 2% per year (which roughly matches the long-run average), and your 9% savings rate stays constant, your annual ringgit savings grow over time too. A more realistic compound model:

| Years of disciplined shopping | Conservative real return (6%) |

|---|---|

| 20 years | RM 18,300 |

| 30 years | RM 41,800 |

| 40 years | RM 85,900 |

So the “realistic 6% real return, 40 years of disciplined shopping” number is closer to RM 85,900 rather than RM 70,000. The optimistic scenarios all scale proportionally upward.

The key insight: time and discipline turn small per-month numbers into life-changing per-decade numbers. RM 35 saved monthly is not a meaningful amount. RM 35 saved monthly, invested for 40 years, is a small fortune. The arithmetic of compound returns punishes inaction and rewards even the smallest consistent contribution.

This is exactly what the old saying captures: sikit-sikit, lama-lama jadi bukit. A little, over time, becomes a hill. The Malaysian wisdom is the same as the math.

Part 6: How to actually do this in real life

Here’s the practical part — what actually works for Malaysian households trying to capture these savings.

How to actually do this

Total setup time: 15 minutes. Then it runs on autopilot.

Part 7: Why almost no Malaysian does this

Here’s what’s interesting: the numbers above are not a secret. The math is simple compound interest. The grocery price data is publicly available. The EPF, ASB, and PRS systems exist and are widely advertised. There is no information barrier to any of this.

And yet almost no Malaysian household actually does it.

The reason isn’t ignorance. It’s friction. Each of the steps above takes a small amount of effort. And each small amount of effort, compounded across thousands of decisions a year, adds up to just enough effort to make most people not bother. So they default to the same store they’ve always shopped at, paying RM 11.25 for a chicken when RM 6.91 is available, and they tell themselves “RM4 doesn’t matter.”

But every RM4 not saved today is RM 60 not present in your retirement account in 40 years, after compound growth. Multiply that across every grocery trip, every week, every year, and the cost of comfortable shopping habits becomes the difference between an average retirement and a comfortable one.

The household that figures this out in their 20s ends up materially wealthier than the one that doesn’t — without earning any more money. That’s the quiet, slightly uncomfortable truth that this analysis surfaces. Personal finance is mostly behaviour, not income.

A summary you can show your spouse

If you take nothing else from this article, take these five lines:

- A household earning RM 7,500/month spends roughly RM 400/month on groceries-at-home — less than most assume.

- Default-shopping at the cheapest store in your area saves about 9%, or RM 35/month / RM 425/year.

- If invested for 40 years at 6% real returns: RM 70,000–86,000.

- If invested at 8% nominal: RM 119,000.

- The whole strategy requires 15 minutes of setup once, plus auto-investing the savings.

If your spouse isn’t convinced, show them the chicken price gap — RM 6.91 versus RM 11.25 in the same district on the same day. That single image is the entire argument.

Sikit-sikit, lama-lama jadi bukit.